TradeEnabler - SWIFT Evolved

SWIFT Evolved: Trust Signal Oracle for Decentralized Correspondent Banking and Decentralized Custody

Executive Summary

The future of regulated finance is not a choice between traditional banking and blockchain. The future is the intelligent integration of trusted financial infrastructure with programmable settlement, decentralized custody, and compliance that is embedded before execution. SWIFT already provides one of the most trusted and widely adopted infrastructures in global finance. The opportunity is not to replace SWIFT, but to extend its reach and utility into the next generation of settlement and real-world asset custody.

The financial industry is facing two misunderstood problems. The first is the breakdown of correspondent banking access, particularly for smaller financial institutions, emerging-market banks, money service businesses, and institutions in jurisdictions perceived as higher risk. The second is the absence of a strong institutional model for decentralized custody of real-world assets. Today, digital asset custody is often framed as a choice between self-custody and centralized custody. Neither model is sufficient for regulated real-world assets, sovereign instruments, or bank-grade settlement.

The common misconception is that cross-border payments are slow because SWIFT is slow. That is incorrect. SWIFT messaging is fast, secure, standardized, and deeply embedded across global banking infrastructure. The real delay in many cross-border payment flows comes from correspondent banking structure, compliance duplication, risk aversion, and the economic imbalance that makes smaller correspondent relationships unattractive to large global banks. A small or emerging-market institution may generate limited fee revenue while requiring the same level of AML, sanctions screening, fraud monitoring, operational controls, and regulatory oversight as a much larger institution. In many cases, the perceived risk is higher while the revenue is lower. This is the real reason de-risking has accelerated.

De-risking is not a symptom of slow payment technology. It is a structural economic and regulatory imbalance. Large global banks have rationally exited many correspondent relationships because the risk-reward equation does not support maintaining them. The result is financial exclusion. Smaller institutions lose access to global settlement. Businesses and individuals in emerging markets face higher costs and fewer options. In response, market participants increasingly use stablecoins and informal digital rails because those networks are available, fast, and less constrained by institutional gatekeepers. This is not a failure of SWIFT as a messaging network. It is a signal that access to correspondent banking has broken down.

TradeEnabler’s Trust Signal Oracle provides a path to solve this problem inside the regulated financial system. It enables decentralized correspondent banking within the SWIFT ecosystem by allowing regulated institutions to settle directly with approved peers, while compliance, identity, risk, and execution rules are validated before settlement. SWIFT messages such as ISO 20022 pacs.009, and where appropriate legacy flows such as MT202, can continue to act as familiar initiation channels. The transformation occurs behind the scenes, in the settlement and validation layer, without forcing banks to abandon their existing systems, workflows, applications, or SWIFT connectivity.

This is the key adoption advantage. Banks do not need to learn a new crypto rail. They do not need to rebuild their payment operations. They do not need to force their staff into unfamiliar blockchain workflows. They can continue to use the infrastructure they already trust, while the Trust Signal Oracle adds programmable compliance, wallet governance, transaction authorization, and settlement control outside the core banking system. This creates a decentralized validation layer that can approve or block settlement before execution.

The second major opportunity is decentralized custody with accountability. Real-world assets, particularly sovereign-backed instruments, require more than self-custody and more than centralized exchange custody. They require institutional-grade custody, regulated accountability, controlled distribution, verifiable ownership, and the ability to interact with public blockchain ecosystems without losing governance. The Sovereign Gold Reserve Token, or SGRT, is a flagship example of this model.

SGRT is not a speculative crypto asset. It is designed as a sovereign-backed real-world asset and monetary instrument. Its architecture can combine SWIFT DLT for institutional custody and transfer between regulated custodians, banking platforms for client distribution and managed exposure, and public blockchain infrastructure such as XDC for direct ownership, programmability, and public accessibility. The Trust Signal Oracle provides the common control layer across these environments, ensuring that ownership, custody, compliance, and transfer rules remain consistent.

This creates an independent validation layer that operates outside core banking systems, capable of approving or blocking settlement before execution. The asset can remain under regulated institutional control while ownership and economic exposure can be distributed across banks, corporates, funds, and eventually individuals or businesses. It allows SWIFT to capture both sides of the future: payments and assets.

For SWIFT, this is not simply a defensive response to crypto networks. It is an expansion opportunity. By enabling decentralized correspondent banking and institutional custody of real-world assets, SWIFT can increase network usage, attract institutions that previously saw limited value in SWIFT membership, support corporate treasury innovation, and provide regulators with stronger tools for oversight, monetary policy support, and risk-based supervision. For banks, it creates a way to reduce correspondent friction, expand settlement relationships, and participate in digital assets without leaving regulated infrastructure. For regulators, it offers a framework where transactions can be governed before execution instead of investigated only after the fact.

TradeEnabler’s Trust Signal Oracle therefore positions SWIFT not only as a messaging network, but as a trusted foundation for programmable settlement, decentralized correspondent banking, and accountable custody of real-world assets.

Author: Hervé Lacorne, Founder & Chairman, TradeEnabler and Founder & CEO, Winstant Limited

1. The Misunderstood Problem

The debate around cross-border payments is often framed incorrectly. Many discussions start from the assumption that the existing financial infrastructure is old, slow, and therefore must be replaced by blockchain-native networks. This assumption misunderstands both the strength of SWIFT and the real source of friction in correspondent banking.

SWIFT is not the bottleneck in cross-border payments. SWIFT messages can move quickly and reliably. Banks around the world already trust SWIFT as a secure communications network, a standards body, and a coordination layer for financial institutions. The infrastructure is embedded into bank operations, treasury systems, compliance workflows, and global financial processes. This makes SWIFT extremely valuable, not obsolete.

The bottleneck is the structure of correspondent banking. Cross-border settlement often depends on networks of correspondent relationships, nostro and vostro accounts, multiple intermediaries, duplicated compliance checks, and risk-based decisions by large global banks. The payment instruction may move quickly, but the settlement process is affected by the ability and willingness of institutions to maintain correspondent relationships and accept the risk of processing transactions for smaller or higher-risk-perceived counterparties.

The problem became more severe after major enforcement actions and large penalties imposed on global banks for compliance failures. Large financial institutions learned that a correspondent banking relationship with a smaller institution could generate modest revenue while exposing the bank to significant regulatory, reputational, and financial crime risk. The economics became unfavorable. A small correspondent relationship may require the same monitoring infrastructure, due diligence, sanctions screening, and review process as a large relationship, while producing only a fraction of the revenue. In higher-risk jurisdictions, the perceived exposure can be even greater.

From the perspective of a large global bank, exiting these relationships can be rational. From the perspective of the global financial system, however, the result is damaging. Smaller institutions lose access. Emerging-market corridors become underserved. Businesses face higher costs. Local banks lose relevance in cross-border activity. Customers search for alternatives.

This is the real reason stablecoins such as USDT have become useful in many markets. The attraction is not that stablecoins are inherently better regulated or safer. The attraction is that they are available, fast, liquid, and not constrained by the same correspondent banking access problem. This should not be understood as a warning sign against SWIFT. It should be understood as a warning sign for regulators and banks that regulated access has become too difficult in many corridors.

The solution is not to replace SWIFT with public crypto rails. The solution is to restore access to regulated settlement by enabling financial institutions to settle directly with trusted peers, using programmable deposit tokens and embedded compliance within a SWIFT-connected environment.

2. Why SWIFT Is the Solution, Not the Problem

SWIFT is uniquely positioned because it already provides what most blockchain networks lack: institutional trust, global adoption, standardization, and regulatory familiarity. The banking industry does not need another disconnected network that asks institutions to leave their existing systems behind. It needs a way to use the tools already in place more effectively.

This is why the SWIFT DLT environment is strategically important. A private, permissioned DLT infrastructure connected to the SWIFT ecosystem can offer a trusted environment for settlement, custody, and institutional digital asset activity. It allows financial institutions to explore programmable settlement without abandoning the governance, security, and operational familiarity of SWIFT.

The value of this approach is especially important for smaller institutions. Many smaller banks, regional financial institutions, and MSBs may not see sufficient value in SWIFT membership or SWIFT usage if they cannot access correspondent banking relationships. If SWIFT connectivity does not lead to practical settlement capability, the subscription and integration costs may appear difficult to justify. However, if SWIFT DLT combined with the Trust Signal Oracle enables direct settlement with approved counterparties, then SWIFT becomes more valuable to those institutions. It becomes not merely a messaging service, but a pathway to global settlement access.

This is also important for higher-risk-perceived institutions and jurisdictions. The Trust Signal Oracle can improve the risk-reward equation by providing compliance and identity validation before execution. Instead of relying solely on after-the-fact monitoring, the system can validate whether a transaction, wallet, institution, and recipient are authorized before settlement occurs. This makes the relationship more manageable and potentially more economical.

SWIFT’s existing role as a standards and messaging layer should not be treated as a weakness. It is precisely the reason this model can work. Banks already understand SWIFT. Their systems already connect to SWIFT. Their compliance teams already recognize SWIFT messages. Their treasury operations are built around established processes. A solution that plugs into this environment is far more likely to gain adoption than a solution that asks banks to start again.

The Trust Signal Oracle does not compete with SWIFT. It enhances SWIFT by enabling settlement, custody, and programmable control to operate on top of its existing trusted infrastructure. It enables SWIFT to become a stronger platform for settlement and custody while preserving the trusted infrastructure that banks already rely on.

3. The TradeEnabler Model

TradeEnabler is a programmable financial orchestration framework that connects trade documentation, identity verification, compliance, payments, settlement, and asset control. The core insight behind TradeEnabler is that trade and cash can no longer remain separate silos. There is no trusted trade without payment, and there is no trusted payment without verified context.

In traditional banking, trade finance and cash management have often been managed separately. Trade focuses on documents, invoices, bills of lading, letters of credit, and financing. Cash management focuses on payment flows, settlement, liquidity, and treasury operations. This separation made sense inside legacy bank product structures, but it no longer reflects how digital commerce, tokenized assets, and programmable settlement operate.

TradeEnabler connects these elements into one trusted transaction environment. Documents can be authenticated. Counterparties can be verified. Wallets can be governed. Payment instructions can be linked to verified business context. Settlement can be executed only when identity, compliance, and risk rules have been satisfied.

The Trust Signal Oracle is the orchestration mechanism that makes this possible. It is not simply a compliance plug-in. It is a control and validation framework that can operate across banking systems, SWIFT infrastructure, and blockchain environments. It orchestrates identity validation, zero-knowledge proof authentication, Travel Rule alignment, sanctions and jurisdictional screening, wallet-level governance, transaction-level risk rules, and execution permissions.

A critical feature is that the Oracle operates outside the core banking system. This matters because it creates decentralized validation. The transaction is not approved solely because a bank’s internal system initiated it or because a private key holder signed it. Execution can depend on an independent validation layer that checks whether the transaction is authorized, whether the recipient is approved, whether the wallet is permitted, whether the jurisdictional rules are satisfied, and whether the transaction fits the governance model of the token or institution.

This external validation model is central to both decentralized correspondent banking and decentralized custody. It allows trust to be enforced across systems rather than trapped inside one institution’s core banking environment.

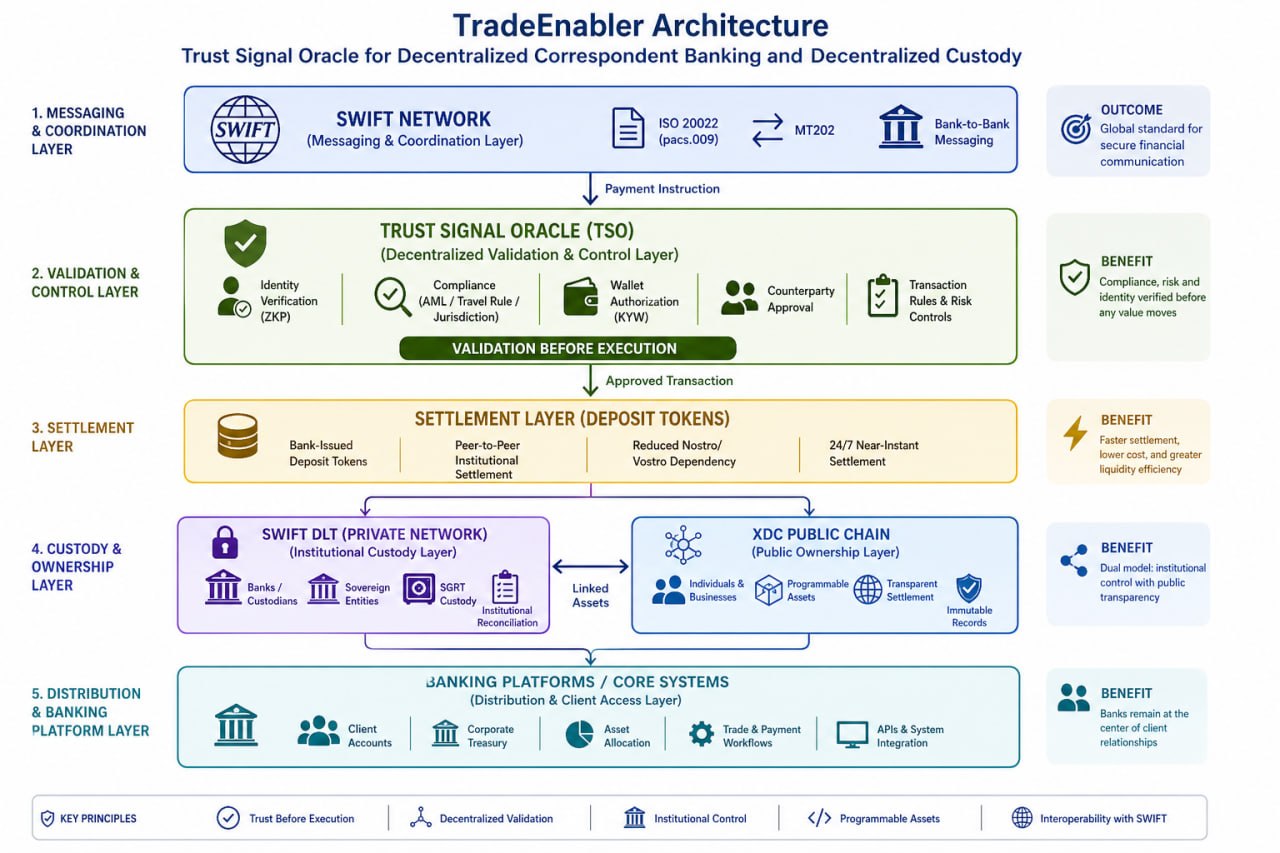

The architecture of TradeEnabler and the Trust Signal Oracle can be understood as a layered integration with existing SWIFT infrastructure, where messaging, validation, settlement, and custody are connected without disrupting existing banking systems.

Rather than replacing SWIFT, this model extends its functionality by introducing a decentralized validation and control layer between payment initiation and settlement, enabling compliance, identity verification, and transaction governance to occur before execution.

The following diagram illustrates how SWIFT messaging, the Trust Signal Oracle, deposit token settlement, and dual custody environments interact to enable decentralized correspondent banking and decentralized custody of real-world assets.

Figure 1 — TradeEnabler Architecture: Integration of SWIFT messaging with the Trust Signal Oracle, enabling validation before execution, tokenized settlement, and a dual custody model combining SWIFT DLT for institutional control and public blockchain (XDC) for ownership and programmability.

4. Decentralized Correspondent Banking

As illustrated in Figure 1, SWIFT messaging continues to act as the initiation layer, while the Trust Signal Oracle introduces a validation layer that enables direct settlement between approved counterparties using tokenized deposits.

The first major application of the Trust Signal Oracle in a SWIFT context is decentralized correspondent banking.

The current correspondent banking model is largely hub-and-spoke. Smaller banks rely on large global institutions to provide access to major currencies and international settlement. This gives large correspondents significant control over access. It also concentrates risk and creates the economic imbalance that drives de-risking.

Decentralized correspondent banking does not mean unregulated banking. It means allowing regulated institutions to establish approved settlement relationships with one another without relying exclusively on large global banks as central hubs. This model can be built inside the SWIFT ecosystem, using SWIFT messaging as the trusted initiation and coordination layer, tokenized deposits as the settlement asset, and the Trust Signal Oracle as the validation and compliance layer.

A bank can initiate a transaction using familiar SWIFT-connected processes. The message may be based on ISO 20022 pacs.009 for financial institution transfers or, during transition, compatible with legacy MT202-style processes. The point is not to force banks to adopt a new front end. The point is to allow existing SWIFT workflows to trigger a faster, governed settlement process.

Before settlement occurs, the Trust Signal Oracle validates the transaction. It can confirm that both institutions are approved participants, that the wallets are authorized, that the transaction is within policy limits, that sanctions and jurisdictional rules are satisfied, and that the recipient is eligible to receive the asset or deposit token. Once validation is complete, settlement can occur using a tokenized deposit or other approved settlement asset.

This model changes the economics of smaller corridors. Instead of relying on a large correspondent bank that may find the relationship unattractive, smaller institutions can settle with trusted peers under a compliance framework that reduces risk and increases transparency. The Oracle does not eliminate the need for regulation. It strengthens regulated settlement by embedding compliance before execution.

The benefit to SWIFT is significant. Institutions that previously saw limited value in SWIFT because they lacked correspondent access now have a reason to participate. SWIFT becomes a platform not only for messaging, but for enabling direct settlement relationships between regulated institutions. This can increase SWIFT traffic, improve network relevance, and support financial inclusion.

5. Deposit Tokens and Settlement Layer

Deposit tokens are a natural settlement asset for this model because they extend the existing banking system rather than replace it. A deposit token represents a bank deposit in digital form. It remains linked to regulated financial institutions and can be structured as an on-balance-sheet liability of the issuing bank.

This distinction is important. Deposit tokens are not speculative crypto assets. They are programmable representations of bank money. They allow banks to modernize settlement while preserving the legal, regulatory, and accounting foundations of deposit relationships.

In correspondent banking, deposit tokens can reduce the need for complex chains of intermediaries and pre-positioned nostro balances. Institutions can settle directly with one another using approved tokenized deposits, while the Trust Signal Oracle ensures that the settlement is authorized and compliant. This can support net settlement between counterparties, faster liquidity movement, and more efficient cross-border flows.

For banks, this creates an opportunity to transform settlement economics. Deposit tokens can make smaller relationships more manageable because compliance can be embedded into the transaction flow. They can also create new revenue opportunities through settlement services, tokenized deposit programs, treasury solutions, and digital asset custody.

For corporates, deposit tokens can improve treasury operations. Corporate treasurers need faster movement of funds, better liquidity visibility, and more precise control over payments. Programmable deposits can support conditional payments, automated sweeps, intercompany transfers, escrow-like arrangements, and liquidity optimization across jurisdictions.

This should not be understood as requiring corporates or banks to become blockchain experts. The strongest adoption path is one where existing banking and SWIFT-connected systems remain in place, while programmable settlement happens behind the scenes. The user experience can remain familiar while the settlement layer becomes faster and more intelligent.

6. Programmable Money and Multi-Layer Governance

Programmable money creates capabilities that traditional cash management systems cannot easily deliver. Today, corporate cash management platforms can support approvals, limits, signatories, and account structures such as zero balance accounts. However, these controls are typically centralized within a bank’s platform and do not naturally extend across public chains, private DLT environments, multiple institutions, and external custody systems.

The Trust Signal Oracle allows governance to operate across environments. Control can be applied at the asset level, the wallet level, the institution level, and the transaction level. This creates a richer model of programmable money.

At the asset level, a token can carry rules about who may hold it, where it may move, and what conditions must be satisfied before transfer. At the wallet level, a corporate or institution can define its own authorization rules, such as dual control, transaction limits, approved recipients, or treasury policies. At the Oracle level, external validation can ensure that compliance and jurisdictional requirements are met before execution. At the settlement level, the transaction can be blocked, delayed, approved, or escalated according to rules.

This is more than multi-signature control. Multi-signature protects against unilateral action by requiring multiple keys. The Trust Signal Oracle adds a separate dimension: the transaction must also be valid under the governance rules. Even if a key is compromised, the system can prevent an unauthorized transfer if the recipient is not approved, the transaction violates policy, or the wallet lacks the required Trust Signal credential.

This is particularly important for institutions and corporates. In traditional finance, access control, maker-checker workflows, dual authorization, and treasury policies are essential. In many blockchain systems, possession of the private key is effectively control of the asset. That is not acceptable for institutional adoption. The Trust Signal Oracle allows blockchain-based assets and tokenized deposits to inherit the control logic expected in corporate cash management while adding decentralized validation across systems.

This creates a stronger cybersecurity model. To compromise a transaction, an attacker would need more than access to a key. The attacker would also need to satisfy external wallet credentials, recipient authorization, Oracle validation, and governance rules. This materially improves the security profile of digital settlement.

7. Decentralized Custody: The Missing Model

Digital asset custody is often presented as a binary choice. Either the user self-custodies the asset, accepting full responsibility for keys and operational risk, or the user relies on a centralized custodian, trusting a single institution or platform to safeguard the asset.

For many crypto assets, this binary framing may be acceptable. For real-world assets, sovereign-backed instruments, regulated financial products, and institutional settlement assets, it is not enough.

Real-world assets require a custody model that can reconcile legal ownership, beneficial ownership, institutional custody, public transparency, regulatory accountability, and controlled transfer. A gold-backed sovereign instrument, for example, cannot be treated like a purely speculative token. It must be governed. It must have credible custody. It must be auditable. It must support institutional distribution. It must also be capable of interacting with public blockchain environments where individuals and businesses may hold or transfer value.

The Trust Signal Oracle enables a third model: decentralized custody with institutional accountability.

In this model, regulated institutions can maintain custody and control of assets while ownership and economic exposure can be distributed. A bank or institutional custodian may hold or reconcile the asset at the institutional level. Clients may receive exposure through banking platforms, managed accounts, corporate treasury systems, or public blockchain wallets. The Oracle ensures that transfer rules, ownership validation, compliance obligations, and recipient authorization are consistently enforced.

This model combines the strengths of centralized custody and self-custody while reducing the weaknesses of both. It provides institutional control without trapping assets entirely inside one custodian. It provides distributed ownership without relying only on private key possession. It creates accountability without exposing sensitive identity information publicly.

This is where SWIFT DLT can become strategically important. SWIFT’s private, permissioned environment can support institutional custody and transfer between regulated entities, while public blockchains such as XDC can support broader accessibility, transparency, and programmability. The Trust Signal Oracle becomes the bridge that allows these environments to work together under a consistent governance framework.

8. Sovereign Gold Reserve Token: Flagship Use Case

The Sovereign Gold Reserve Token, or SGRT, is a flagship use case because it demonstrates both dimensions of the model: decentralized correspondent settlement and decentralized custody of a real-world asset.

SGRT is designed as a sovereign-backed real-world asset and monetary instrument. It is not merely a tokenized commodity or speculative digital asset. Its value proposition depends on regulated custody, sovereign accountability, asset verification, institutional participation, and controlled distribution. This makes it an ideal example of why SWIFT DLT, XDC, and the Trust Signal Oracle can be combined.

The institutional layer can be built around SWIFT DLT. In this environment, regulated institutions, sovereign entities, banks, and approved custodians can hold, transfer, reconcile, and manage SGRT at the institutional level. This provides privacy, control, and institutional-grade governance. Ownership between custodians can be recorded and managed within a trusted permissioned environment.

This is important because institutions require privacy. A bank, fund, or sovereign entity may not want all custody and allocation details exposed on a public chain. SWIFT DLT can provide the private institutional environment needed for custody, reconciliation, and regulated transfer.

At the same time, SGRT also benefits from public chain accessibility. XDC can provide transparency, programmability, and direct ownership for individuals, businesses, and non-institutional participants outside the SWIFT ecosystem. Public blockchain infrastructure can allow SGRT to circulate in broader economic use cases, while still being governed by the same Trust Signal Oracle logic.

Banking platforms provide a third distribution channel. A financial institution may custody SGRT at the institutional level and then distribute exposure to clients through its own platform, similar to how banks custody securities, gold, Bitcoin, or other assets while offering client-level balances or accounts. The bank can distinguish between its own holdings, client holdings, managed accounts, fund allocations, and corporate treasury positions. The underlying institutional custody can remain reconciled, while client access is delivered through familiar banking interfaces.

This creates a unified model. SWIFT DLT supports institutional custody and transfer. Banking platforms support distribution and client access. XDC supports public ownership and programmability. The Trust Signal Oracle ensures that each environment remains governed by identity, compliance, jurisdictional rules, wallet credentials, and recipient authorization.

As illustrated in Figure 1, SGRT uses the same layered architecture: SWIFT DLT supports institutional custody and transfer, banking platforms provide client-level distribution, and the XDC public chain enables broader ownership and programmability. The Trust Signal Oracle acts as the common governance layer across all three environments, ensuring that custody, ownership, compliance, and transfer rules remain consistent.

The cybersecurity advantage is substantial. In a conventional token model, control of the private key can be enough to move the asset. In the SGRT model, key possession alone is not sufficient. The transfer must also satisfy Oracle validation, wallet-level governance, recipient authorization, and jurisdictional rules. This makes unauthorized transfers significantly harder and provides institutions with a digital asset model closer to the control expectations of traditional finance.

For SWIFT, SGRT demonstrates how its infrastructure can support more than payments. It shows how SWIFT DLT can become part of the institutional infrastructure for real-world assets. This expands SWIFT’s relevance into tokenized sovereign instruments, regulated commodity-backed assets, and future institutional asset classes.

9. Corporate Treasury and Programmable Financial Control

Corporate treasury is a major beneficiary of programmable settlement. Corporates need faster liquidity movement, better control over cross-border flows, and stronger safeguards against fraud. They also need systems that integrate with their banks rather than forcing them to operate directly on unfamiliar blockchain networks.

A SWIFT-connected programmable settlement environment can allow corporates to manage liquidity more intelligently. Corporate funds can move between accounts, subsidiaries, jurisdictions, and counterparties according to predefined rules. Payments can be conditional. Treasury policies can be enforced before execution. Wallet-level controls can reflect corporate approval structures.

The Trust Signal Oracle allows corporates to extend traditional cash management rules into digital settlement. A corporate may require dual approval for large transfers, restrict payments to approved counterparties, impose jurisdictional limits, require additional validation for high-risk transactions, or use wallet-level governance to manage operational risk. These rules can operate independently from the bank’s core system while still being integrated with bank and SWIFT infrastructure.

This is important because corporate cash management today is often centralized within a bank platform. The Trust Signal Oracle enables a more decentralized model where the corporate, the bank, and the Oracle can each contribute to transaction governance. Execution can require alignment across multiple systems rather than relying on a single platform or key.

For banks, this creates a new service opportunity. Banks can offer programmable treasury, tokenized deposit settlement, digital asset custody, and controlled corporate wallets without asking clients to self-custody assets or operate directly on public chains. Banks remain central to client relationships while offering modern capabilities.

For SWIFT, corporate treasury use cases increase network relevance. SWIFT can support not only interbank messages, but also programmable settlement workflows that connect banks, corporates, custodians, and real-world assets.

10. Cybersecurity and Trust Architecture

Cybersecurity is one of the strongest arguments for the Trust Signal Oracle model. In blockchain environments, assets can move quickly and irreversibly. This is powerful, but dangerous if control depends only on private keys. Institutional finance requires more robust safeguards.

The Trust Signal Oracle introduces layered security. A transaction is not valid simply because a key signs it. The Oracle can require that the wallet has the correct credential, the recipient is authorized, the transaction complies with policy, the institution is approved, and the jurisdictional requirements are satisfied. This is a major improvement over systems where key compromise can lead directly to asset loss.

This architecture brings blockchain closer to traditional financial control environments. Banks and corporates are accustomed to approval hierarchies, delegated authorities, sanctions controls, transaction monitoring, and exception management. The Oracle allows these concepts to be applied to tokenized deposits and real-world assets.

The security model also supports privacy. Zero-knowledge proof can allow identity and compliance attributes to be verified without exposing unnecessary personal or institutional data publicly. This is particularly important for transactions involving institutions, sovereign entities, and high-value assets. Participants can remain private to the public while accountable through regulated channels.

In the SWIFT context, this is especially valuable. SWIFT already provides trusted private communications between financial institutions. The Trust Signal Oracle extends that trust into execution. It allows compliance and authorization to be embedded in settlement without placing sensitive information on a public chain.

This also supports regulators. Instead of relying only on after-the-fact investigation, regulators can benefit from systems where compliance conditions are checked before execution and audit trails exist for authorized review. This strengthens the integrity of digital asset markets and payment flows.

11. Strategic Impact for SWIFT, Banks, Corporates, and Regulators

The strategic impact of this model is broad because it addresses payments, custody, settlement, compliance, and financial inclusion at the same time.

For SWIFT, the model expands relevance. SWIFT can capture both sides of the future: payments and assets. It can increase usage among institutions that previously saw limited value because correspondent banking access was constrained. It can support real-world asset settlement and custody within a trusted institutional environment. It can also respond to the rise of crypto rails without abandoning the regulated financial system.

For banks, the model creates new capabilities without requiring a disruptive technology migration. Banks can continue using existing SWIFT connectivity and internal systems while offering faster settlement, tokenized deposit programs, programmable treasury services, and institutional digital asset custody. Smaller banks can regain access to international settlement. Larger banks can reduce operational risk by relying on embedded compliance and pre-transaction validation.

For corporates, the model offers more control over money and assets. Treasury operations can become faster, more programmable, and more secure. Corporates can benefit from bank-provided digital asset and deposit token services without becoming blockchain operators.

For regulators, the model offers stronger oversight. Transactions can be designed to distinguish between domestic and cross-border flows, apply different governance rules, and preserve privacy while maintaining accountability. Regulators can gain better visibility into regulated digital settlement without pushing activity into informal or offshore crypto channels.

This also creates a subtle but important monetary policy benefit. By making regulated digital settlement more efficient, governments and regulators can encourage financial activity to remain within supervised institutions. They gain better tools for oversight, financial inclusion, and systemic stability, without framing the model as anti-dollar or anti-existing reserve currency structures.

12. SWOT Analysis

Strengths

The primary strength of the model is that it builds on trusted infrastructure rather than replacing it. SWIFT already has global recognition, adoption, and institutional credibility. Banks already connect to SWIFT and understand its role. This dramatically reduces adoption friction compared to new blockchain-native networks.

Another strength is the ability to preserve existing bank workflows. Banks do not need to change their applications, user interfaces, or operational processes to benefit from programmable settlement. The transformation occurs in the settlement and validation layer.

The Trust Signal Oracle adds a major compliance and cybersecurity advantage. It enables identity validation, wallet governance, recipient authorization, and pre-transaction compliance. This makes tokenized settlement more acceptable to banks, corporates, and regulators.

The SGRT use case adds a second strategic strength. It shows that SWIFT DLT can support institutional custody of real-world assets, not only payments. This gives SWIFT a pathway into asset infrastructure.

Adoption Challenges

The primary challenge is education. Banks and regulators must understand that the model does not replace SWIFT and does not require uncontrolled crypto exposure. It enhances existing regulated infrastructure.

Liquidity design is also important. Deposit token settlement requires clear rules for issuance, redemption, netting, finality, and liquidity management. These are solvable issues, but they require careful institutional design.

Bank adoption can be slow because financial institutions are conservative. The long transition to ISO 20022 shows that even message-level changes can take time. This reinforces the importance of a plug-in model that minimizes workflow disruption.

Opportunities

The biggest opportunity is decentralized correspondent banking. SWIFT can become more valuable to institutions that currently lack access to correspondent relationships. This can increase participation and network traffic.

A second opportunity is institutional real-world asset custody. SWIFT DLT can become a trusted private environment for sovereign-backed instruments, tokenized commodities, and future regulated asset classes.

A third opportunity is corporate treasury transformation. Banks can offer programmable treasury services through familiar platforms while using tokenized deposits and Oracle governance behind the scenes.

A fourth opportunity is regulatory alignment. The model gives regulators better tools for oversight, pre-transaction compliance, and monetary policy support.

Threats

The primary threat is continued migration to crypto rails if regulated institutions do not provide faster and more accessible settlement. Stablecoins will continue to fill gaps where correspondent banking fails.

Another threat is regulatory misunderstanding. If tokenized deposits and real-world asset tokens are treated as speculative crypto rather than extensions of regulated financial infrastructure, adoption could slow.

Cybersecurity remains a threat in any digital settlement environment. This is precisely why the Trust Signal Oracle’s control architecture is necessary.

13. Conclusion

SWIFT is not the problem in cross-border payments. The problem is the structure of correspondent banking, the economics of de-risking, and the absence of a trusted model for decentralized custody of real-world assets.

TradeEnabler’s Trust Signal Oracle provides a practical path forward. It allows SWIFT to evolve from trusted messaging into trusted programmable settlement and custody infrastructure. It enables regulated institutions to settle directly with approved peers, using tokenized deposits and embedded compliance. It enables sovereign-backed real-world assets such as SGRT to operate across SWIFT DLT, banking platforms, and public blockchain infrastructure such as XDC.

This model does not ask banks to abandon their systems. It makes their existing systems more valuable. It does not ask regulators to accept uncontrolled crypto rails. It gives regulators better tools for oversight and pre-transaction governance. It does not bypass SWIFT. It extends SWIFT into both payments and assets.

The result is a more inclusive, more secure, and more programmable financial system. Smaller institutions can regain access. Corporates can gain better treasury tools. Banks can expand services. Regulators can preserve oversight. SWIFT can strengthen its central role in global finance.

The future is not about replacing trusted financial infrastructure. It is about making that infrastructure programmable, accountable, and accessible.